How the EU Grids Package Can Succeed

The package will not move until Member States agree on how grid costs are shared, congestion income allocated, and planning authority distributed.

- 1 Introduction

- 2 Brief overview of the EU Grids Package

- 3 Where do countries mostly agree?

- 4 Where do disagreements and key pain points lie?

-

5

Five compromises to unlock the package

- 5.1 Planning governance: Give the scenario process legitimacy, not a veto

- 5.2 Congestion income: Carve out domestic congestion income first

- 5.3 Cost allocation: Extend cost-sharing scope and incentivise fairer distribution

- 5.4 Permitting: Calibrate permitting without weakening safeguards

- 5.5 Financing: Deploy funds more catalytically

Executive Summary

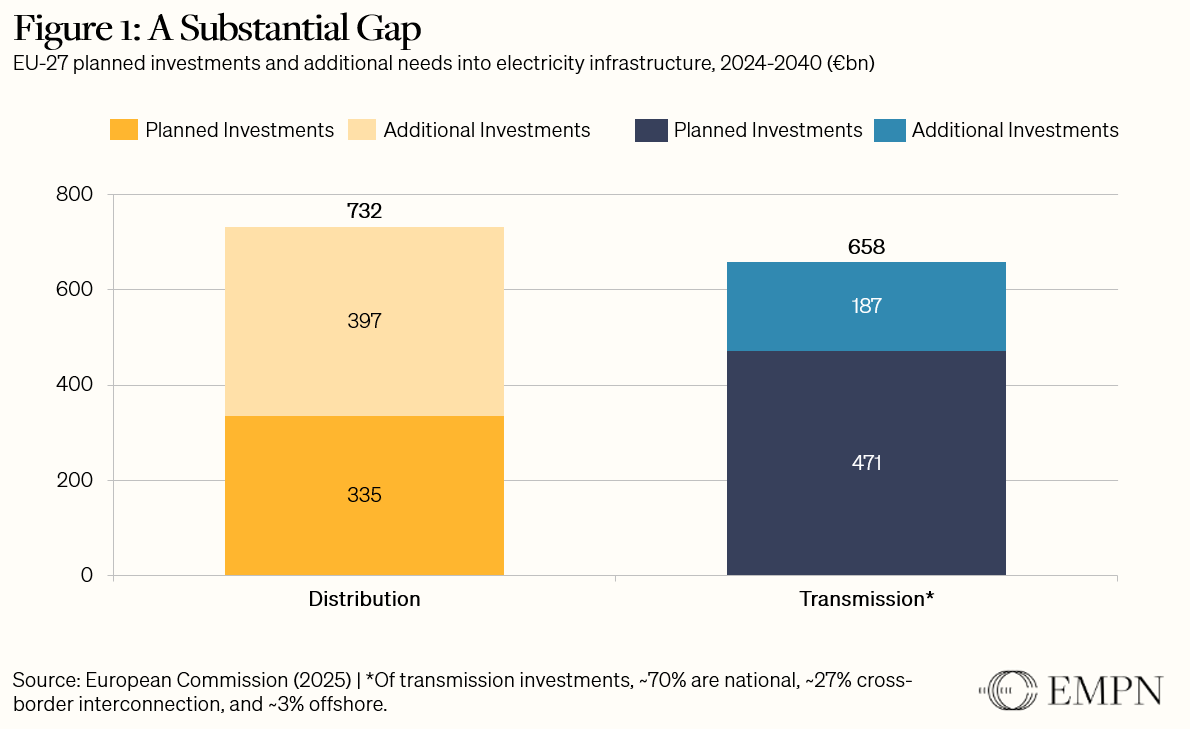

Europe’s grid infrastructure deficit has become a strategic liability. A strong and interconnected European energy system is the most cost-effective way to scale the continent’s renewable and electrification share, thereby reducing fossil imports and lowering energy prices. Yet almost half of the EU’s cross-border electricity capacity needs for 2030 remain unaddressed.

The EU Grids Package is the Commission’s bid to unblock grid investment. Launched in December 2025, the package aims to fast-track permitting, shift infrastructure planning towards EU-level steering, mandate cross-border cost allocation proportional to benefits, and require TSOs to earmark 25% of congestion income for EU cross-border projects – a provision that effectively redirects often domestically generated revenues towards cross-border infrastructure.

Member States broadly agree on direction, but disagreement persists. While the strategic case for grid expansion commands broad support, disagreements over infrastructure planning, congestion income, and cost-sharing reflect four structurally divergent national coalitions. Transit countries (e.g., France and Austria) bear domestic grid costs from cross-border flows and want compensation. Mid-to-high-price importers (e.g., Germany and Poland) expect cheaper electricity imports. Low-to mid-price exporters (e.g., Sweden and Finland) fear higher prices through enhanced interconnection. Low-to-mid-price importers (e.g., Denmark and Belgium) support integration, with some anticipating a shift towards net exporter status.

Compromise is within reach but requires concessions on all sides. The Cypriot Presidency compromise moves in the right direction but falls short of the deeper distributional concerns driving opposition. Five targeted measures, addressing Member States’ red lines and creating room for compromise, could unlock the deal.

Key Recommendations

- Increase the process legitimacy of the central scenario. The central scenario should remain a delegated act, but built through a transparent, co-developed process with mandatory sensitivity analysis. Gap-filling tenders by the Commission should only apply where Member States have already agreed in principle but delivery is stalled by maturity or financing constraints.

- Carve out domestic congestion income. Mandatory earmarking should apply only to cross-border congestion income, with limited international use of the funds only where a Cross-Border Cost Allocation (CBCA) demonstrates significant benefit to the country in question. Member States meeting the EU’s interconnection target should retain full discretion. This also avoids creating a disincentive against bidding zone reform, which the proposed rule risks introducing.

- Extend cost-sharing to transit-driven domestic grid reinforcements. Domestic grid costs linked to cross-border flows should be eligible for CBCA via a dedicated assessment mechanism. Amortisation vehicles and guidance on tax mechanisms can improve distributional outcomes.

- Calibrate permitting without weakening safeguards. Tacit approval should apply only where national law allows. Cross-border project timelines should be aligned across Member States.

- Deploy public financing first and target it better. Extend the scope of CEF-E funding to transit-driven domestic reinforcements and target the funding towards projects with asymmetric cost-benefit profiles among participants, bundled projects, and projects with large spillovers to third party countries. Mobilise EIB and national development banks before defaulting to costlier private arrangements.

1. Introduction

Europe’s electricity grid sits at the intersection of three converging imperatives: transition, competitiveness, and security: Reaching the EU’s 2030 and 2040 renewable energy and electrification targets requires approximately EUR 1.4 trillion in grid investment to harness complementary energy sources and avoid curtailing energy production – yet nearly half of the EU’s cross-border electricity capacity needs for 2030 remain unaddressed (Finesso et al. 2025).

This gap not only puts the EU’s climate targets at risk but also contributes to high energy prices and fossil fuel dependency. Deeper interconnection and more coordinated infrastructure planning could save Europe over EUR 560 billion between 2030 and 2050 (Fraunhofer IEG et al. 2025). A strong and interconnected energy system is the precondition to substantially increase Europe’s renewable and electrification share – thereby reducing fossil imports (European Commission 2025a). Both the war in Iran and the resulting disruption of global energy markets are a stark reminder: as long as Europe remains dependent on imported hydrocarbons, geopolitical crises will translate into economic crises at home.

Against this backdrop, the European Commission launched its EU Grids Package on 10 December 2025, describing grids as the “backbone of the European energy system” (European Commission 2025b). The package aims to close the infrastructure gap by centralizing planning, accelerating permitting, and aligning compensation and financing across Member States (MS) – addressing both the domestic grid deficit within countries and the lack of cross-border interconnection among them. That gap is substantial: 41 of the 88 GW of cross-border electricity capacity needed by 2030 remain unaddressed, with the shortfall projected to grow to 108 GW by 2040 (European Commission 2025c).

Yet translating shared strategic ambition into coordinated action remains deeply contested – particularly when national interests, sovereignty concerns, and divergent energy profiles collide at the Council table. As the debates among MS examined in this paper make clear, the question is not whether Europe needs a more integrated grid – on that, there is broad agreement –, but whether the EU Grids Package creates the right conditions and incentives for MS to actively support its build-out. Aligning divergent national interests with the EU-level integration agenda is the political task at the heart of negotiations.

Resolving negotiation challenges is the focus of this paper. It argues that the EU Grids Package is unlikely to be adopted before the end of 2026 without addressing a set of deeply contested questions: who controls infrastructure planning and how much steering authority the EU can legitimately exercise; how the costs and benefits of cross-border integration are distributed among MS; and whether the financing mechanisms create genuine incentives. The national responses to the proposal reflect tensions that go beyond technical disagreements. They are, at their core, political ones. Any workable solution requires a political bargain that addresses divergent national interests over deeper energy system integration.

The following chapters map where that bargain is possible and where the current text stands in its way. To inform this analysis, we draw on close collaboration with our European Macro Policy Network (EMPN) partner institutions in Denmark, Finland, France, Germany, the Netherlands, and Sweden. Together, they reflect important parts of the EU’s diverse energy landscape in terms of electricity prices, renewable shares, export capacities, and exposure to cross-border cost implications. Their insights are complemented by broader desk research on all EU MS and the wider energy policy landscape, including analysis of the public session of the Transport, Telecommunications and Energy (TTE) Council Meeting on 16 March 2026.

The paper is structured as follows: Chapter 2 provides an overview of the EU Grids Package’s key provisions. Chapter 3 identifies areas of broad agreement among MS. Chapter 4 elaborates on the main disagreements and pain points of MS. Chapter 5 outlines potential avenues for solutions.

2. Brief overview of the EU Grids Package

The EU Grids Package aims to enable a cost-efficient, competitive, and secure energy system at EU level. It comprises five elements, of which the first three are legislative instruments and the last two are non-binding guidance documents:

- proposed revision of the Trans-European Networks for Energy (TEN-E) Regulation, setting the framework for cross-border energy infrastructure planning, project selection, permitting, and cost-sharing among MS (European Commission 2025c);

- a proposed Directive to accelerate permit-granting procedures, amending the Renewable Energy Directive, the Electricity Market Directive, and the Gas Market Directive to streamline and shorten authorisation procedures across MS (European Commission 2025d);

- the Energy Highways Initiative, identifying priority cross-border corridors for accelerated financial support, covering electricity interconnections, offshore wind, gas resilience, hydrogen transport, and price stability in South-East Europe (European Commission 2025e);

- a non-binding guidance document on efficient grid connections, introducing the “first-ready, first-served” principle to streamline access and reduce delays in connecting new generation capacity (European Commission 2025f);

- a non-binding guidance document on two-way contracts for difference, providing a common design framework to support investment certainty for renewable energy generators across the EU (European Commission 2025g).

While the non-binding guidance documents raise few political concerns, the TEN-E revision has proven far more contentious. Four aspects shape the political debate in particular: who controls infrastructure planning, whether the EU can determine how Transmission System Operators (TSO) use congestion income, who bears the costs of infrastructure build out, and whether the EU can override national permitting decisions:

Planning. Noting that fragmented, bottom-up planning has led to distinct and at times misaligned investment priorities across MS, the Commission (2025c) proposes to take on a stronger role in central planning. Based on the TEN-E revision, it would be empowered to develop a central, cross-sector scenario covering electricity, hydrogen, and gas on a four-year cycle (Art. 11). This scenario then becomes the reference for needs assessment, cost-benefit analysis, and PCI/PMI selection (Arts. 12, 14), while MS, TSOs and European Networks of Transmission System Operators (ENTSOs) provide input to the Commission. Where the Commission identifies infrastructure gaps that are not addressed by existing project proposals, it would gain the authority to launch a “gap-filling” process which, if no suitable project proposals emerge, could ultimately empower the Commission to tender for the construction of interconnectors directly – without requiring the agreement of the MS concerned (Art. 12, 13). Overall, this represents a shift from the TYNDP’s bottom-up logic to a top-down approach by the EU.

Congestion Income. Seeking to mobilise additional financing for interconnector projects that are currently falling behind their targets, the Commission (2025c) proposes a further provision for TSOs under Article 19 of the TEN-E revision TSOs would be required to earmark 25% of their total congestion income for investment in Union list projects aimed at reducing interconnector congestion – though the proposal leaves open whether these funds would be deployed at a MS’ own borders or anywhere across the EU. The earmarked income is to be held in a separate account until either deployed or until it can be demonstrated that no additional cross-border capacity is required. Notably, the conditions governing the use of these funds would be further specified by the Commission via a delegated act. In practice, this provision effectively transfers control over TSO revenues to the Commission.

Cost-sharing. Cross-border energy infrastructure generates benefits that extend well beyond the country hosting or financing it, but existing frameworks have not adequately ensured that beneficiary countries contribute to its costs. The Commission (2025c) therefore revises the cross-border cost allocation (CBCA) framework to embed a clearer beneficiary-pays principle. Under these revised rules, costs would be allocated in proportion to the benefits received, with a 10% benefit threshold triggering mandatory participation in a project (Art. 17). Agreements must be reached ex-ante, and project bundling allows multiple Union list projects – including domestic “internal lines” – to be assessed jointly (Arts. 17–18). Eligibility for Connecting Europe Facility for Energy (CEF-E) funding under Article 21 is contingent on three conditions: demonstrated positive externalities, a prior cost allocation decision as indicated under Article 17, and an inability to attract market financing where a project is simply not economically viable.

Permitting. Considering that slow permitting remains one of the most significant barriers to infrastructure deployment, the TEN-E revision introduces a tacit approval mechanism whereby a project is deemed approved if a national authority fails to respond within a defined deadline (European Commission 2025c). Target timelines are set at up to two years for most projects and a maximum of three years for the most complex cases (Art. 10). Projects on the Union list – currently comprising 235 PCIs and PMIs (European Commission 2025h) – further benefit from streamlined environmental assessments (Art. 7), consolidated reporting (Art. 9), and clearer pre-application rules (Art. 10). These TEN-E revision is complemented by the Commission (2025d) proposed Permitting Directive streamlining measures to the broader energy infrastructure landscape, including domestic grids, storage, and renewables beyond the Union list.

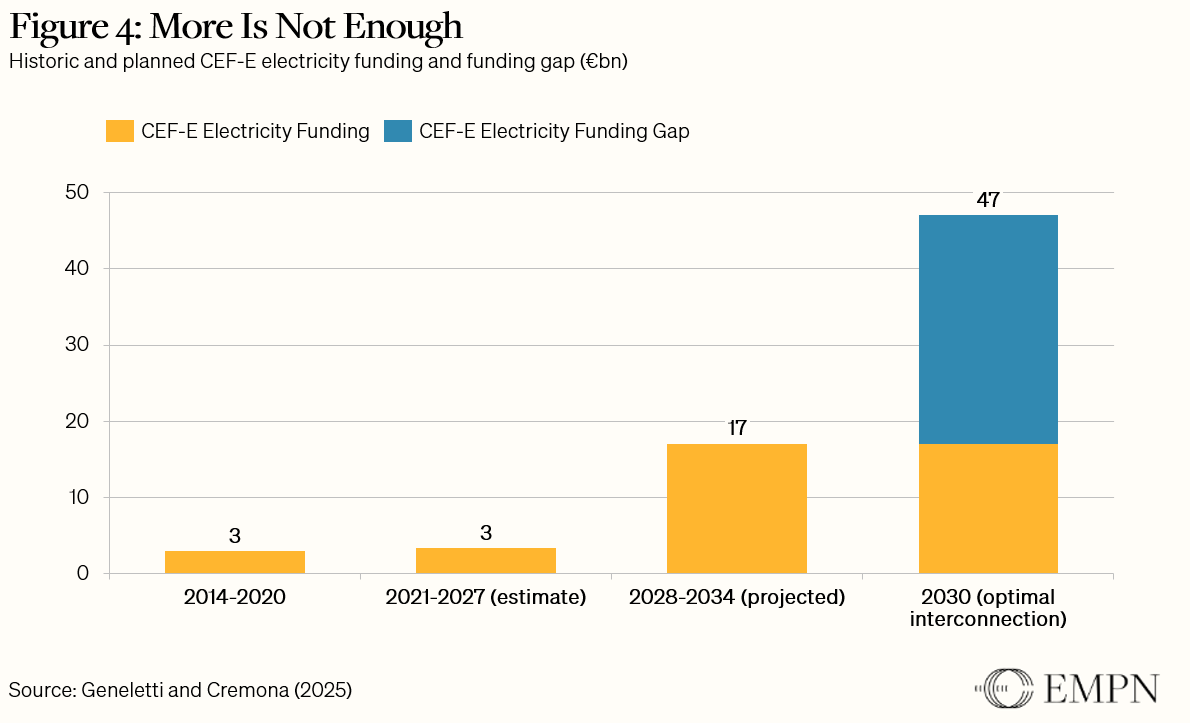

While the EU Grids Package does not directly address financing, the Commission (2025i) has introduced two instruments that frame its broader investment context. First, it proposes a fivefold increase of the CEF-E – from EUR 5.84 billion (2021–2027) to EUR 29.9 billion (2028–2034) under the next Multiannual Financial Framework (MFF). Second, through the Clean Energy Investment Strategy (CEIS), published in March 2026, the Commission (2026) intends to leverage the European Investment Bank (EIB) that will deliver EUR 75 billion over three years for energy infrastructure investments, deployed via equity platforms, securitisation facilities, hybrid bonds, and intermediated lending.

As the costs of upfront investments not covered by CEF-E grants will be recovered through network tariffs – falling on consumers and grid users –, the financing implications of the EU Grids Package make it particularly sensitive for MS, as Chapter 4 outlines.

3. Where do countries mostly agree?

Despite the significant disagreements examined in the following chapter, the EU Grids Package is generally considered to be a necessary and timely initiative. The March TTE Council (2026) confirmed that MS share common ground on the package’s general direction, even where they diverge sharply on its specific provisions.

As such, we identify four main areas of agreement:

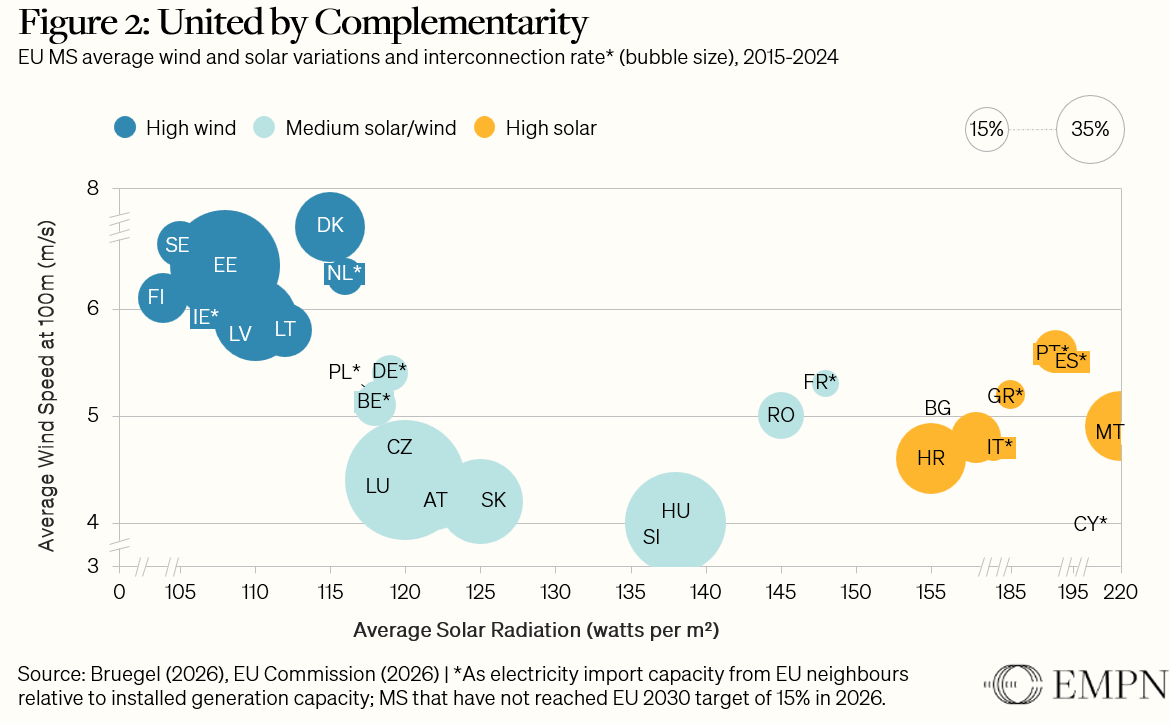

More grid investment is needed. EU electricity prices remain roughly twice those in the United States and China and price disparities within the EU itself are large – with Central and Eastern Europe (CEE) facing structurally higher prices due to insufficient access to western European electricity markets (Eurostat 2026). Romania pointed to EUR 4.2 billion in total congestion costs; Croatia noted that even well-connected countries with high renewable shares still face elevated spot prices (TTE Council 2026). At the same time, wind-rich northern regions and solar-abundant southern regions stand to gain from better cross-border balancing (Roth et al. 2026, see Figure 2). While individual MS differ on how much additional interconnection is desirable and on what terms, no MS questions the fundamental premise that Europe’s grids need to be expanded and modernised. Greece went as far as calling a common European energy market “a must” (TTE Council 2026).

Accelerated permitting is a shared priority. Slow permitting was identified across the Council (2026) as a binding constraint on infrastructure deployment. As such, Germany noted that grid infrastructure takes seven to nine years to plan, whereas renewables projects take two. This contributes to EUR 3 billion in German redispatch costs per year, as renewables in the North must be paid to switch off, while power plants in the south ramp up production. There is broad consensus that the package’s ambition to shorten timelines and streamline procedures is the right approach, even as MS diverge on the details of implementation – including tacit approval, environmental safeguards, and the balance between EU-level deadlines and national procedural flexibility.

Strengthened energy security is a shared concern. Overall, MS welcome that the Commission has made infrastructure resilience upgrades eligible for CEF-E funding. For Baltic and Nordic MS, recent infrastructure sabotage in the Baltic Sea has made resilience a dominant concern shaped primarily by geopolitical exposure. For peripheral and island MS like Malta, Ireland, and Cyprus, energy security is above all a question of basic connectivity. Larger, more integrated MS like Germany and the Netherlands frame energy security in systemic terms: a means to manage periods of Dunkelflaute or to reduce residual fossil fuel dependency. Put simply, access to abundant wind-, solar- and hydropower resources in certain parts of Europe secures an agreement among MS and alleviates their high dependency on energy imports from elsewhere.

Stronger EU co-financing is accepted in principle. The proposed fivefold increase of CEF-E is broadly welcomed, and no MS argued against the principle of EU co-financing for infrastructure with cross-border benefits. At the Council (2026), the Czech Republic called for annual CEF-E calls and Finland described CEF-E as “an excellent tool” (TTE Council 2026) for facilitating cross-border investments. At the same time, MS emphasise that stronger financing must go hand in hand with fairer cost allocation. This is where apparent consensus fractures: agreement on the principle of EU co-financing coexists with deep disagreement over who bears its distributional consequences – a tension that runs through each of the contested provisions examined in the following chapter.

4. Where do disagreements and key pain points lie?

As concluded above, the strategic direction of the EU Grids Package is broadly shared: MS recognise the urgency of grid expansion, the need for faster permitting, and the case for EU-level financing. However, the March 2026 TTE Council (2026) debate confirmed that significant disagreements persist – ranging from fundamental questions about EU-level planning authority to specific provisions like the 25% congestion income rule.

We identify five areas of contention:

4.1. Planning governance: Who sets the scenario?

The proposed TEN-E revision shifts infrastructure planning towards stronger EU-level steering. The Commission (2025c) would take over the development of a central scenario for the electricity, hydrogen, and gas sectors, replacing the current bottom-up process in which ENTSOs and TSOs drive scenario development with MS and stakeholder input. This scenario becomes the reference point for the TYNDP, the infrastructure needs assessment, and PCI/PMI selection. Critically, the Commission also gains “gap-filling” powers: where identified cross-border capacity needs are not matched by project proposals from MS and their TSOs, the Commission may launch an open call for proposals to any third party capable of acting as a project promoter (Arts. 12–13).

MS disagreement on this point concerns the scope and legitimacy of central steering. The breadth of the coalition raising concerns is striking. At the March 2026 TTE Council (2026), France, Sweden, Germany, and Finland all voiced fundamental objections, while Poland, Slovakia, Czech Republic, Italy, Belgium, Lithuania, Hungary, and Slovenia raised concerns of varying intensity about the single-scenario approach, the weakening of their TSOs’ role, or both.

Two distinct critiques emerge beneath this broad opposition:

The first is institutional: Lithuania, Slovakia, Slovenia, Poland, Czech Republic, Hungary, France, and Italy fear that centralised scenario-setting weakens the role of TSOs in network planning and detaches the process from the technical expertise that underpins credible infrastructure decisions. Lithuania argued that the TYNDP cycle should remain at two years rather than four, and that TSOs should remain responsible for technical modelling within the policy framework set by the Commission. Slovakia went further, questioning why the Commission should assume the central role at all, warning that centralisation risks complicating governance rather than simplifying it (TTE Council 2026).

The second critique is substantive: At the Council (2026), France, Sweden, Belgium, Germany and Hungary question whether a single central scenario can provide sufficient granularity, arguing it focuses too heavily on the supply side while neglecting demand-side dynamics and national specificities. France calls for multiple scenarios developed cooperatively by the Commission, MS, and TSOs, arguing that a single centralised scenario introduces a rigidity incompatible with the agility required by energy markets. Sweden argues that planning must be as close to consumption as possible, making bottom-up the guiding principle – a view shaped by the reality that Sweden’s electricity needs vary sharply between its industrial north and its more densely populated south. Belgium explicitly stated that “a single centralised scenario is not the best option” and called for a variety of players to be involved. Hungary called for clear approval and amendment rights for MS, National Regulatory Authority (NRA), and TSOs – not just over data, but over modelling assumptions and parameters affecting their own territory. Germany, on the other hand, emphasises the need for additional scenarios based on regional input, given that demand growth varies significantly across its planning regions and that TSO and Distribution System Operator (DSO) level planning must be coordinated jointly (TTE Council 2026).

Although MS did not explicitly invoke the gap-filling mechanism by name at the TTE Council (2026), Malta stated that decisions on infrastructure needs and how these gaps are addressed should be decided at a national level, in full respect of the subsidiarity principle. Finland insisted that MS must retain the right to decide whether cross-border infrastructure is needed at all. Beyond the Council (2026), recent reporting by Politico (2026) suggests that for France and Sweden the governance provisions are potentially deal-breaking – with officials from both countries described as “pushing to kill” the EU Grids Package. As such, the Commission’s gap-filling power is a direct challenge to the principle that national TSOs control what gets built on their territory.

Overall, a small group of MS – Greece, Spain and Romania –expressed comfort with a strong Commission-led planning role: In specific, Greece called a common European energy market a “must” and “sine qua non“, and dismissed critics’ confrontational tone outright: “ultimatums are not the way to operate right now.” Spain stressed the Iberian Peninsula’s need to stop being an “energy island”, while Romania pointed to “less bureaucracy, less procedure, less time getting approvals” (TTE Council 2026).

4.2. Congestion income: Who controls generated revenues?

Among the specific provisions in the EU Grids Package, the requirement for TSOs to earmark 25% of their congestion income for projects on the Union list (Art. 19) has provoked the broadest and most intense opposition (European Commission 2025c).

Congestion income arises from electricity price differences across borders and internal bidding zones._ It is substantial, unevenly distributed across MS, and currently used by TSOs largely at their discretion, often to reduce domestic network tariffs (ACER 2026). The Commission’s rationale for earmarking is straightforward: congestion signals infrastructure bottlenecks, so a share of the income should fund their resolution. But for MS that have already invested heavily in interconnection or that generate large congestion rents from internal bottlenecks rather than cross-border constraints, the provision amounts to a financial transfer that penalises past investment and good practice.

At the TTE Council (2026), opposition was overwhelming. Sweden’s intervention was the most dramatic: the Swedish energy minister Ebba Busch disclosed that the Swedish TSO collected EUR 3 billion in congestion revenues in 2024, of which 75% arose from internal bottlenecks and not cross-border interconnectors. She described the provision as “simply unacceptable” (TTE Council 2026) for countries that lead the way in clean energy exports and bidding zone reform, declared it a “hard red line,” and explicitly threatened a moratorium on new interconnections to continental Europe if the direction does not change – warning of “harsher and further actions” (TTE Council 2026). The political context matters: Sweden is holding general elections in September 2026, and energy prices are expected to be a key issue (Büscher & Dimitrisina 2025).

Austria, Belgium, Finland, Hungary, Latvia, Lithuania, Poland, and Slovenia all expressed opposition or strong reservations at the Council (2026). Hungary argued that redistributing congestion income “could undermine the original investment logic and the legitimate expectation of benefits” (TTE Council 2026). Slovenia – whose cross-border capacity was built with Slovenian consumer contributions and stands at over 200% of installed capacity – stated that “taking away the benefits of this cross-border integration from the people, now after they have paid for it, will not be well accepted” (TTE Council 2026). Finland insisted that congestion revenues should be used “where they were created” (TTE Council 2026) to ease the bottlenecks causing the revenues in the first place. Lithuania opposed the use of delegated acts to set conditions for congestion revenue use, insisting that key rules must be established directly in the regulation. Ireland called for further analysis of the provision’s impact on consumer prices.

Only Bulgaria, Romania, and Croatia expressed support, albeit for different reasons. Romania and Croatia, as high-price importing countries, stand to benefit from accelerated cross-border investment financed partly through congestion rents from elsewhere. Bulgaria, by contrast, may benefit from improved export capacity, noting its large share of domestic solar energy.

4.3. Cost allocation: WHo Bears Which costs?

At the heart of the distributional debate is the question of who bears the financial consequences of enhanced interconnection. When electricity markets with different price levels become interconnected, electricity typically flows from lower-price to higher-price markets. This increases domestic prices in exporting countries and reduces them in importing ones, thus reducing energy supplier rents. Moreover, the resulting cross-border flows can overload domestic grids in transit countries, requiring costly national reinforcements to handle electricity that neither originates nor terminates within their borders. While there may be a net benefit at the system level – coordinated infrastructure planning could save Europe over EUR 560 billion between 2030 and 2050 (Fraunhofer IEG et al. 2025) – the distributional effects can be uneven.

The March 2026 TTE Council (2026) confirmed that MS positions towards cross-border expansion are largely shaped by these distributional effects: Countries that expect net welfare gains from deeper interconnection broadly support the proposals, while those facing higher domestic prices, transit costs, or threats to their existing energy mix are more cautious or opposed.

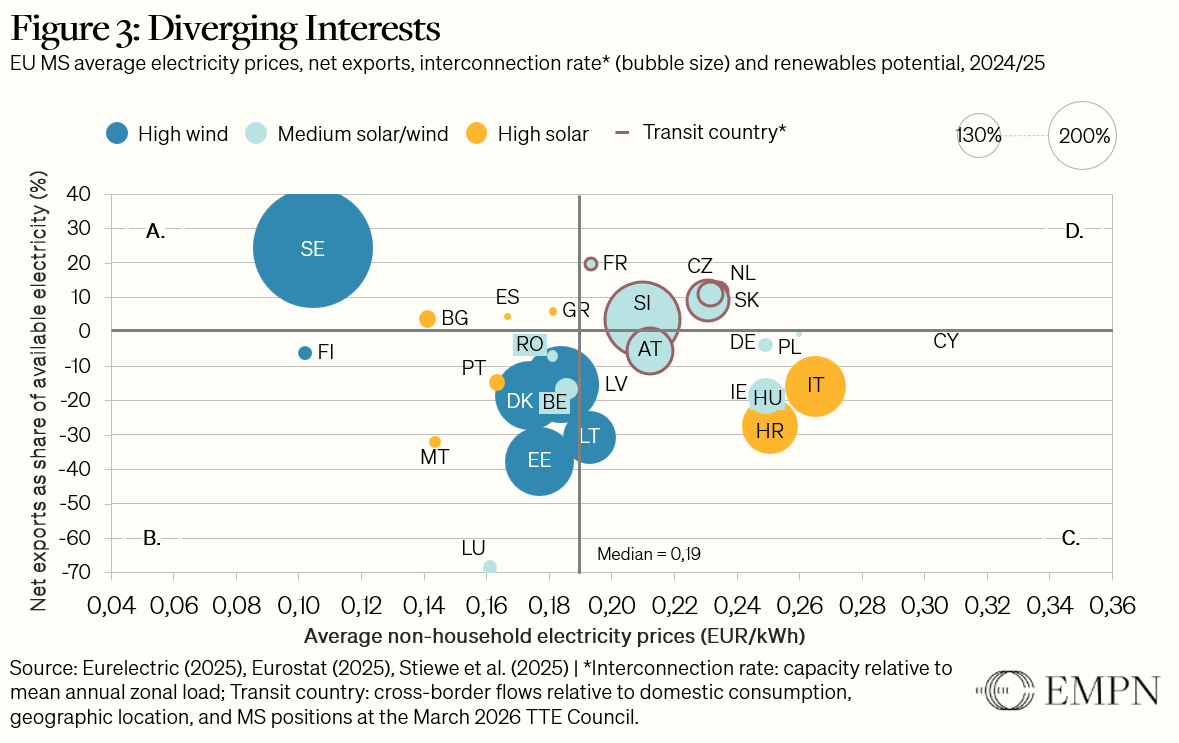

There are at least four structural factors that influence a MS’s position: its current wholesale electricity price level, its status as net exporter or importer, its current interconnection rate, and its renewable energy potential (Eurelectric 2025; Eurostat 2025). Figure 3 provides an overview.

While structural factors prevent a clean categorisation of MS positions, they help explain these divergences. The EU Grids Package will itself shift MS positions over time – as deeper integration turns some exporters into importers and vice versa. On average the price level should fall, but for some MS it may increase as prices converge – in the absence of corrective measures. This structural uncertainty makes the net benefits for each individual MS difficult to assess, underpinning the political challenges in the ongoing negotiations.

A. Low-to-mid-price exporting countries, including Spain, Greece, Bulgaria, and Sweden will likely see rising power prices because of deeper interconnection. Yet their positions vary greatly, shaped by each MS’s interconnection headroom and the role grid stability plays in their energy transition. Spain and Greece are strongly in favour: both have low interconnection rates and high solar potential, leaving them under-connected relative to their generation capacity. For these solar-dependent systems, deeper interconnection is not merely an export opportunity but a structural necessity – providing access to dispatchable power from neighbouring markets during periods of low solar output and, with it, a crucial source of grid stability.

On the other hand, Sweden, which has the highest interconnection rate among MS, fears that further interconnection would raise domestic prices in southern Sweden, which is already paying higher prices than in the more northern price zones. This could be a consequence of larger continental demand for its power generated by hydro and nuclear generators, off synch with renewables elsewhere. A recent study on the halted Hansa PowerBridge II project between Germany and Sweden finds interconnection gains accrue disproportionately to producers – whose low-cost hydro and nuclear capture higher marginal prices – while consumers face losses. Asymmetric cost-sharing alone is insufficient to offset these consumer losses (Emelianova et al. 2025).

B. The picture is somewhat different for low-to-mid-price importing countries, including Belgium, Denmark, Finland, Portugal, and Romania among others. As net importers, most of these MS are open to deeper integration. Romania points to the fact that CEE countries “were getting the highest prices in the entire EU because there is no very clear access to the western market” (TTE Council 2026). Finland is an exception and more sceptical, which follows from its very low electricity prices. Similar to Sweden, extended interconnection could result in higher prices in the medium term. Some MS in this group, including Denmark, Portugal and the Baltic countries, may become future net exporters in a more deeply integrated European market thanks to extensive wind or solar resources.

C. Mid-to-high-price importing countries mostly include MS from Central and South-Eastern Europe, e.g. Austria, Germany, Poland, Hungary and Italy, and most are supportive in general. Germany, in particular, expects to benefit from cheaper European imports, noting that its energy prices are among the highest in the EU and continue to pose a major challenge to its competitiveness and core industries. Except for Croatia and Italy, MS in this group have medium solar and wind potential.

D. Finally, mid-to-high-price-exporting countries including the Czech Republic, France, Austria, the Netherlands, and Slovakia share two characteristics: these MS are all “transit countries” today or will become so in the future, and none of them relies solely on wind or solar in their current or projected energy mix. In practice, these MS bear higher domestic grid costs driven by electricity flows that neither originate nor terminate within their borders – a structural inequity that the current regulatory framework does not adequately address. At the TTE Council (2026), Austria – where transit accounts for 70% of electricity traffic – argued that “the development of national energy infrastructure cannot be supported solely by national actors” and called for new financing instruments to distribute risks fairly. Slovakia further argued that the costs of cross-border interconnections “should not be fully covered by consumers in the transit country” (TTE Council 2026).

Among the mid-to-high-price countries, France’s situation is unique: With a nuclear share in power output of roughly 65%, extended integration to Spain risks a surge of cheap renewable imports driving down spot prices and undermining the economics of its nuclear fleet. Moreover, while France’s overall wind and solar potential is moderate on average, the country benefits from complementary regional resources – strong winds in the North and East, and high solar irradiation in the South. France is also concerned that greater interconnection will increase its domestic grid reinforcement needs and drive up congestion, particularly in view of the high congestions in the South of Germany. Together, this explains France’s low interconnection rate today and its position that “cost-sharing has […] to lead to strengthening the network so that the energy travels better within the country” (TTE Council 2026).

The proposed CBCA reform attempts to address some of these tensions through ex-ante cost allocation proportional to benefits, a 10% benefit threshold triggering mandatory participation by non-hosting countries, and the possibility of project bundling including domestic “internal lines” (Art. 18). However, several MS argue these reforms do not resolve two more fundamental problems:

The first concerns the scope of cost allocation. The core problem is that the CBCA framework under Article 17 allocates costs based on net benefits received but does not recognise the costs imposed on transit countries whose domestic grids carry transit flows. France’s case is concrete: large-scale transit of Iberian electricity to Germany and Central Europe would load the French grid, requiring domestic reinforcements whose costs fall entirely on French consumers and are not eligible for cross-border cost allocation. While Article 18 bundling could in principle allow internal lines with significant cross-border impact to access the CBCA, the framework does not specify under what conditions transit-driven domestic reinforcement costs become cost-sharing eligible. That gap is unresolved. Separately, Article 17 contains an explicit carve-out excluding loop flow mitigation from CBCA – meaning that even where a project reduces unscheduled cross-border flows that load third-country grids, this cannot form the basis for cost allocation to affected TSOs. Taken together, the framework recognises cross-border benefits in terms of energy flows received, but not infrastructure costs imposed by flows passing through.1

The second concerns the link between cost-sharing and domestic reform. Sweden and Finland take the position that credible national reforms must accompany expanded interconnection – including restructuring bidding zones in countries with significant internal congestion. Sweden’s energy minister opened her Council intervention with the statement: “we’ve done our homework, like really” – pointing to Sweden’s internal bidding zones, near-100% fossil-free electricity, and status as the EU’s largest per capita net exporter.

What is more, Sweden’s intervention points to a deeper issue: domestic reforms and fairer cost-sharing must go hand in hand. The Hansa PowerBridge II case illustrates why: as mentioned, the asymmetric cost-sharing alone cannot offset Swedish consumer losses under the current market configuration. Although a German bidding zone split would change the calculus entirely – eliminating the need for additional transfers –, it is very unlikely that this domestic reform in Germany is unlikely to materialise in the near term. In fact, the bidding zone split remains politically contested due to its price implications for southern industry in Germany. The result is a perverse dynamic: Sweden, which has already undertaken domestic reforms, finds itself penalised rather than rewarded, while the countries that have not reformed face no comparable pressure.

4.4. Permitting: Acceleration by any means?

Permitting is the area of broadest agreement. Virtually all MS recognise that slow permitting is a binding constraint on grid deployment and support the package’s ambition to accelerate procedures. Germany’s minister noted that it takes seven to nine years to plan grid infrastructure, whereas photovoltaic (PV) parks take two. However, reaching a consensus on the overall direction does not necessarily lead to a consensus on the specifics.

Three points of contention emerged at the TTE Council (2026).

First, tacit approval of permits is contested. The provision – under which permits are deemed granted if authorities fail to decide within the deadline – was criticised by Austria (which sees “significant risks”), Bulgaria (which called for exceptions covering all stages of environmental assessment), and the Netherlands (which argued that tacit approval was deliberately abolished in Dutch law in 2024 because it leads to “unclear permits with unclear conditions” and conflicts with decision-making requirements). The Netherlands thus suggest making tacit approval optional (TTE Council 2026).

Second, nearly all MS insisted on maintaining strong environmental safeguards, with many warning against creating sector-specific permitting regimes that could fragment the regulatory landscape. Ireland argued for a “clear, streamlined and consistent approach across different sectors” rather than bespoke regimes. Finland stated how “numerous proposals containing exceptions are leading to fragmentation and increasing complexity” (TTE Council 2026).

Third, the balance between EU-level procedural requirements and national administrative realities remains unresolved. Several MS raised concerns about the combined effect of the mandatory two-year permitting deadline, the single competent authority model, and the digital portal requirements. Together, these provisions impose uniform procedural templates on administrative systems that differ significantly across MS. Italy noted that its multi-level administrative system makes the Commission’s approach of “semi-yearly changes to legislation” (TTE Council 2026) problematic. Belgium argued in favour of MS’ flexibility to choose tools “better adapted to their national realities” (TTE Council 2026). Germany stressed that EU regulations “should support and not counteract national acceleration measures” (TTE Council 2026), flagging specific tensions with the Water Framework Directive and the Soil Monitoring Directive.

4.5. Financing: How to pay for grids expansion?

Beyond the specific provisions of the TEN-E revision, MS positions on the broader financing framework remain fragmented.

Three tensions stand out:

The first concerns the scale of CEF-E. The proposed fivefold increase – from EUR 5.84 billion to EUR 29.9 billion under the next MFF (European Commission 2025i) – is broadly welcomed, but several MS already consider it high in the context of wider budget negotiations. At the same time, estimates suggest an additional EUR 30 billion gap remains for cross-border expansion alone after accounting for this proposed increase (Geneletti & Cremona 2025), and the Czech Republic called for CEF-E calls to be issued annually to accelerate disbursement. Whether the final MFF lands above or below the Commission’s proposal will directly shape what is achievable on cost-sharing and project delivery.

The second concerns the scope of funding eligibility. Germany and Sweden maintain EU funding should focus on cross-border projects. France takes the opposing view: domestically located but system-critical investments should qualify for EU support precisely because they are driven by pan-European rather than national needs. The TEN-E revision’s provision for project bundling (Art. 18) partially addresses this by allowing internal lines to be assessed jointly with cross-border projects – but it does not specify under which conditions domestic costs become eligible for shared financing, leaving the question operationally unresolved.

The third concerns the financing mix. MS are divided on how to best address the grid financing gap and whether EU-level debt instruments should contribute. Sweden has consistently opposed expanded EU-level borrowing, arguing that growth and capital market reform – including leveraging private savings – should provide the necessary resources (Blenkisop & Martinez 2025). The current government’s stance reflects broader fiscal conservatism: despite supporting public debt-financed nuclear expansion domestically, Sweden shows no inclination to support EU-level debt instruments for grid investment. Denmark has earlier emphasised the role of the EIB in keeping financing costs low for grid expansion and shielding consumers from tariff increases. France has signalled greater openness to common EU debt, with President Macron publicly backing Eurobonds (Caulcutt & Leali 2026). In Germany, the debate is shifting at the margins – the President of the Bundesbank has expressed openness to common financing instruments – but the Merz government remains opposed, meaning no common German position has emerged (Sigmund 2026). The CEIS, with its focus on mobilising private capital through securitisation, hybrid bonds, and equity platforms, represents the Commission’s current approach. Nonetheless, several MS and the broader macroeconomic debate point toward a larger role for public finance than the current framework envisions.

These financing questions will not be resolved within the EU Grids Package itself – they depend on the MFF negotiations, the evolution of the Savings and Investments Union, and broader political choices about fiscal integration.

4.6. Diverging interests: overview

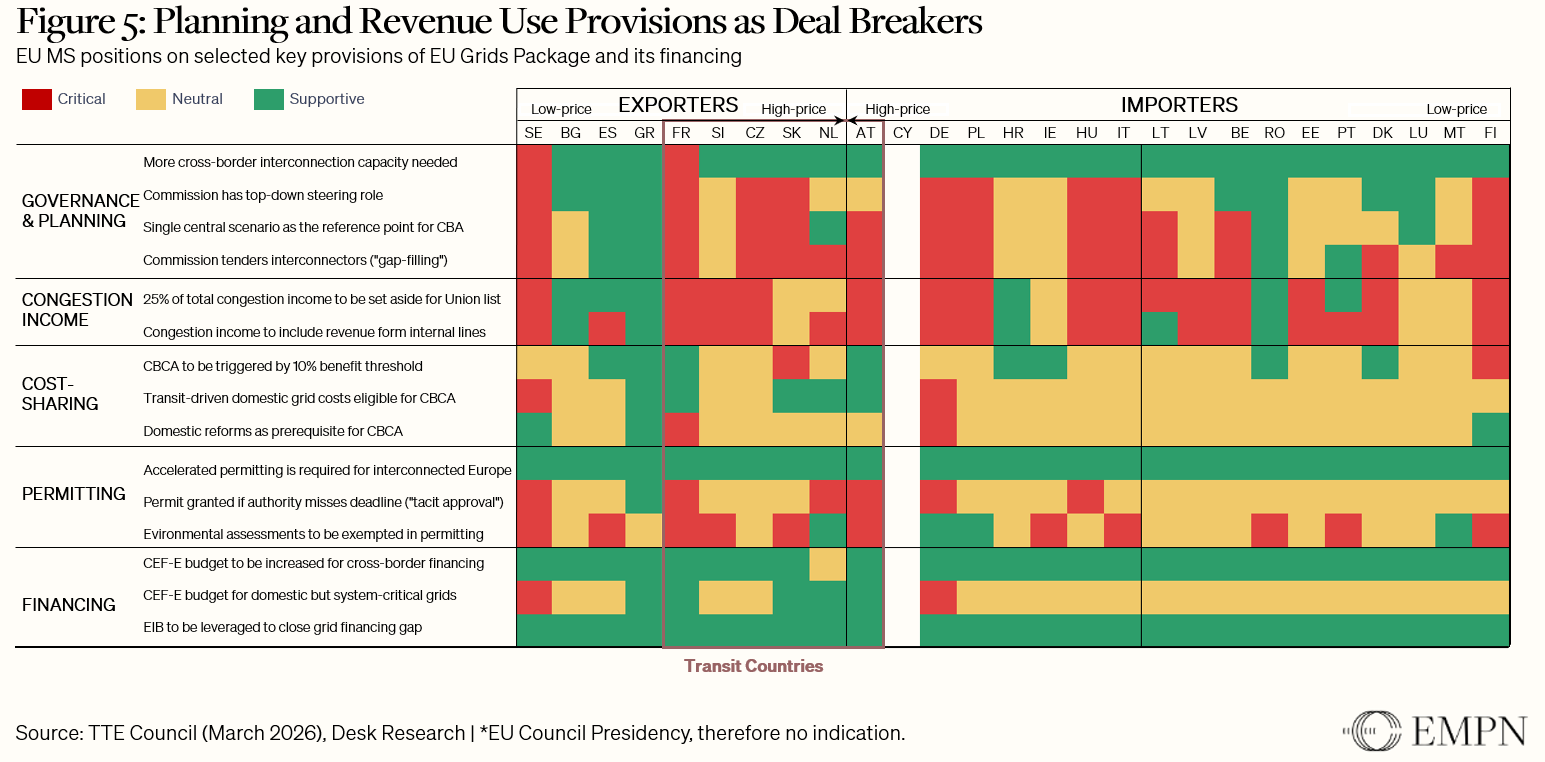

The March TTE Council (2026) revealed broad unity on the strategic case for grid expansion, faster permitting, and stronger EU-level financing – yet deep division on the provisions determining who controls infrastructure planning and who bears the financial consequences of deeper integration. The coalitions that emerge around these disagreements are not accidental – they reflect structural differences in MS energy profiles, interconnection rates, and exposure to price convergence, as discussed in this chapter.

As Figure 5 illustrates, disagreements break down along five lines:

- the legitimacy of Commission-led scenario planning

- the mandatory earmarking of congestion revenues

- the degree of domestic reforms required for CBCA

- the acceleration of permitting procedures

- the eligibility of domestic grids for CEF-E funding.

Resolving these disagreements requires targeted compromises on each of the contested provisions, as the following chapter outlines.

5. Five compromises to unlock the package

The previous chapter identified five areas of disagreement. In this chapter, we outline possible avenues for compromise in each of these areas and address the proposed TEN-E and Permitting Directive revision of the legal texts by the Cypriot Council Presidency.

5.1. Planning governance: Give the scenario process legitimacy, not a veto

MS objections to the governance provisions of the EU Grids Package are not principally about EU-level harmonisation as such – they concern its legitimacy and the risk of national competences being overridden. The Cypriot Presidency (Cypriot Presidency 2026a; 2026b) has attempted to address this by replacing the delegated act for the central scenario with an implementing act, giving MS a formal qualified majority veto. However, this addresses the symptom rather than the cause. Under qualified majority voting, France and Sweden – despite being among the most affected countries – could still be outvoted, as neither commands a blocking minority alone. A scenario adopted over, for instance, French or Swedish objections would be legally valid but practically contested. The more fundamental problem is not MS control over the outcome, but the process that produces it.

A credible central scenario requires a transparent, inclusive process. Bruegel analysts argue convincingly that EU energy system planning currently suffers from a deep transparency deficit: planning relies on opaque, often proprietary modelling whose assumptions cannot be independently scrutinised or reproduced (Roth et al. 2026). Their proposal – an EU Energy Data Hub feeding into open-source energy system modelling managed by a public interest institution, such as the Commission’s Joint Research Centre – addresses these issues. But transparency alone is not sufficient. MS and their TSOs must not be passive data providers to a Commission-run process; they must be active co-developers of the scenario through a structured, iterative exercise in which their inputs visibly shape the output and their objections can be tested against shared evidence. A scenario produced through this process is more likely to reflect EU-wide energy system realities and to command the political trust needed to serve as a genuine reference.

Importantly, the Commission’s proposal does not abolish the TYNDP. In fact, ENTSOs retain responsibility for the TYNDP but must work from the central scenario. This architecture is in principle sensible. A credible EU-level scenario can surface cross-border infrastructure needs that bottom-up national TSOs may not consider themselves. As they plan within national mandates, TSOs may simply not propose projects that fall outside their domestic remit, even if these projects are optimal from a European welfare perspective. The scenario’s added value lies precisely here: not as an enforcement tool, but as a means of expanding the planning horizon beyond what national remits naturally produce.

The central scenario should also always be accompanied by mandatory sensitivity analyses – capturing different demand, technology, and geopolitical assumptions. Planning under a single deterministic scenario creates false precision and locks in assumptions for decades. The Presidency (2026a) compromise retains sensitivity analyses as a possibility but does not make them mandatory. They should be.

If the process is credible, the scenario can remain a delegated act – but its enforcement scope should be limited. A scenario developed through a transparent, co-developed process will command broad political support without requiring a formal MS vote. The delegated act is the appropriate legal instrument, but the central scenario’s role must be clearly bounded: it should serve as the shared analytical basis for cost-benefit analysis (CBA), PCI/PMI selection, the TYNDP, and CBCA negotiations. As such, it can inform and structure negotiations – whether bilateral or multilateral – but it cannot realistically be used to trigger gap-filling calls against MS that have made a deliberate political choice not to build a given project. It is the job of appropriate incentives and updated cost-sharing mechanisms to make these projects happen. Infrastructure built without MS cooperation cannot be enforced. The gap-filling mechanism should only apply where MS have already agreed in principle – through regional cooperation frameworks or TEN-E Group endorsement – but where delivery is stalled due to project maturity or financing constraints.

National planning commitments need to improve, but enforcement should be proportionate. National Energy and Climate Plans (NECPs) remain poorly operationalised and methodologically inconsistent, undermining the quality of national inputs into EU-level planning. Two measures merit consideration: stronger methodological harmonisation requirements so that national inputs are comparable and aggregable, as proposed by Bruegel analysts (Roth et al. 2026); and a “follow-or-explain” requirement whereby MS whose plans deviate materially from the EU’s targets and central scenario must provide a reasoned public justification. Access to certain EU infrastructure funding could ultimately be made conditional on NECP quality, but a follow-or-explain approach is the right starting point and would already represent a meaningful step forward.

5.2. Congestion income: Carve out domestic congestion income first

The mandatory ring-fencing of 25% of congestion income for Union list projects is challenged across virtually all MS, albeit for different reasons: Denmark fears it forces overinvestment in already well-connected MS and that it removes funding reserved for paying for existing interconnectors. Sweden objects to losing its sizeable domestic interconnector fees to European-level priorities, while German TSOs argue for a voluntary approach (50hertz, Amprion, TenneT and TransnetBW 2026; TenneT 2026). Overall, Lithuania, Latvia, Hungary, Poland, and Slovenia principle of mandatory earmarking altogether (TTE Council 2026).

The Presidency compromise – limiting the earmarking to cross-border congestion income as well as restricting the usage to domestic interconnection projects – is a step in the right direction. Beyond addressing understandable MS concerns, carving-out internal congestion income is sensible for another reason: Not doing so would create a perverse incentive against bidding zone reform. Since the earmarking applies to congestion income arising at crossings between domestic price zones, MS may be reluctant to introduce additional bidding zones if this means that the resulting domestic congestion rents must be spent on international projects rather than domestic ones. Sweden – one of only three MS that have introduced national bidding zones – is directly exposed to this dynamic.

A limited extension to cross-border projects outside the hosting MS should be considered. Prioritising domestic Union list projects ensures that congestion revenues remain linked to the system context in which they were generated – a logic that is both economically sound and politically sustainable. However, a rigid domestic-only rule may occasionally foreclose more efficient uses of the funds. Where a CBCA assessment under Article 17 establishes that a cross-border project generates significant benefits for the MS in question – applying the same 10% benefit threshold that triggers mandatory CBCA participation – it is reasonable to allow ring-fenced funds to also be directed towards that project. This preserves the domestic-first principle while opening a targeted and evidence-based pathway to cross-border use, conditional on demonstrated benefit rather than discretion.

Allowing congestion income to be used for domestic internal reinforcements could be sensible – provided demonstrable impact on cross-border flows can be established. A bidding zone split is one such condition where applicable, though not the only one. This would create a targeted incentive for domestic price reforms that improve system efficiency without making bidding zone reform a hard prerequisite.

MS that have met their interconnection targets should retain full discretion over how congestion income is deployed – a principle already implied by the Commission’s TEN-E revision. Retaining this discretion would allow MS to direct congestion income toward either reducing network tariffs or financing the internal grid reinforcements necessary to make existing interconnection capacity fully effective.

5.3. Cost allocation: Extend cost-sharing scope and incentivise fairer distribution

The core challenge regarding distribution and cost-sharing is asymmetry. As such, the MS most likely to face higher grid costs and/or higher electricity prices because of deeper interconnection are also those with the least incentive to agree to the package as currently designed. Any workable solution must therefore take their concerns seriously – while acknowledging that other MS will be reluctant to bear additional costs on their behalf.

The Presidency compromise is silent on cost allocation. The Cypriot TEN-E compromise text makes no substantive changes to the CBCA framework under Article 17: the 10% benefit threshold, the loop flow exclusion, and the absence of any mechanism for transit-driven domestic reinforcement costs all remain unchanged. For MS like France, Austria, and Slovakia – whose core objection is that the package asks them to host cross-border flows without recognising the domestic costs this imposes – the Presidency text offers nothing. Any compromise that leaves this dimension unresolved risks losing the transit country coalition entirely.

We believe that three complementary solutions should be considered, with priority given to those most likely to be implemented quickly. Each solution addresses a different aspect of the problem.

The first and most direct fix is to extend cost-sharing eligibility to domestic grid reinforcements causally linked to cross-border flows. The current CBCA framework allocates costs based on net benefits received but does not account for domestic grid reinforcements that are necessary to enable cross-border flows. The TEN-E revision (European Commission 2025c) already permits project bundling including internal lines under Article 18, yet it does not specify under what conditions transit-driven domestic costs become eligible for cost-sharing.

A dedicated assessment mechanism – evaluating whether new interconnection capacity generates demonstrable additional domestic grid costs, or whether domestic reinforcements would attenuate adverse price impacts – would fill this gap without requiring a fundamental overhaul of existing rules. Where a causal link is established, the associated domestic costs would become eligible for CBCA. For France, which faces substantial transit-driven reinforcement requirements, this would significantly improve the credibility and fairness of the framework. Alternatively, or additionally, internal reinforcements that are necessary to enable cross-border flows could become eligible for CEF-E funding (see below section on financing).

The second fix can address the timing of cost recovery through network tariffs. Two mechanisms serve this purpose: On the one hand, national amortisation vehicles – as proposed by Bruegel – can provide interim financing that absorbs depreciation costs temporarily, allowing cost recovery over longer timelines rather than front-loading costs onto current consumers (Heussaff & Zachmann 2025). The EU could support this initiative by providing design guidelines, while the EIB could reduce the cost of financing these vehicles by offering favourable co-financing rates. On the other hand, non-binding Commission guidance on redistribution mechanisms – combining a time-limited windfall contribution on generators benefiting from improved market access with a corresponding reduction in consumer bills – could help MS manage the political economy of adjustment without requiring a mandatory transfer mechanism (Weber 2023). Assuming that generator surpluses from interconnection can be taxed to benefit consumers and citizens more broadly, increasing price convergence may be viewed positively from a societal standpoint.

A third solution concerns domestic reforms, which should be pursued in parallel with fairer cost-sharing, as it requires long-term commitment from MS. The aforementioned Hansa PowerBridge II study (Emelianova et al. 2025) investigating the economics of interconnection between Sweden and Germany is instructive: a German bidding zone split removes the need for additional cost transfers altogether- However, asymmetric cost-sharing alone, without structural market reform, is insufficient to offset losses for Swedish consumers. Therefore, any solution to the distributional consequences of deeper integration requires a systematic approach.

One way to accelerate domestic reform is to make access to certain EU infrastructure funds conditional upon MS meeting defined energy system efficiency benchmarks. This would ensure that EU support does not compensate for persistent inefficiencies, such as Germany’s single price zone. The independent energy hub proposed in the planning section could develop transparent and comparable benchmarks for this purpose.

Taken together, these three measures would not eliminate the underlying tension over who pays for interconnection – but they would make the cost-sharing exercise more likely to succeed.

5.4. Permitting: Calibrate permitting without weakening safeguards

In terms of accelerating the permitting process, reaching a consensus on the direction does not necessarily mean reaching a consensus on the specifics. Three specific disagreements emerged at the March TTE Council (2026): tacit approval, where Austria and the Netherlands argued the instrument creates legal uncertainty; environmental safeguards, where Ireland and Finland warned against sector-specific regimes that fragment the regulatory landscape; and the combined effect of mandatory timelines, the single competent authority model under TEN-E, and digital portal requirements. Italy, Belgium, and Germany argued that the latter imposes uniform procedural templates on administrative systems that differ significantly across MS.

The Presidency (2026a; 2026b) and, more recently, Niels Fuglsang (2026) in his role as Rapporteur on the EU Grids Package support the Commission’s introduction of tacit approval – though the Presidency takes a more measured approach by making it conditional on its existence in national law. Both also introduce environmental exemptions: the Presidency exempts refurbishment and repowering of existing grid infrastructure, introduces an overriding public interest presumption in Habitats and Birds Directive balancing assessments, and exempts projects from nitrogen assessment. Rapporteur Fuglsang (2026) adds a Water Framework Directive exemption for grid projects on the grounds that grid infrastructure is unlikely to deteriorate water bodies.

While these exemptions are intended to accelerate deployment, they risk generating legal challenges and public acceptance problems that could delay projects more than the procedures they replace – precisely the outcome Ireland and Finland warned against. The Dutch experience illustrates this risk concretely: years of litigation under the Birds and Habitats Directive have repeatedly halted infrastructure projects, not because the directive was misapplied, but because the tension between environmental safeguard and infrastructure needs was never resolved at the level where it originates – EU law itself. This highlights a structural issue that MS discretion cannot resolve while EU environmental directives and infrastructure ambitions are pulling in different directions. Without a clear hierarchy, national courts become the default arbitrator, producing unpredictable results.

A clearer EU-level overriding public interest definition – explicitly establishing that Union list projects take precedence in balancing assessments under relevant environmental directives – would address the legal uncertainty. The governance logic is straightforward: if the EU is responsible for establishing and prioritising permits, it should equally define the boundaries of environmental exemptions – resolving the trade-off once at EU level, rather than 27 times in national courts.

What is more, Rapporteur Fuglsang (2026) suggests that communities affected by grid projects should reap economic benefits, such as reduced electricity bills, resource rents and co-ownership schemes. While this addresses a distinct dimension of public acceptance, it is also relevant to avoiding delays: citizens and NGOs may be less likely to take legal action if they understand and benefit directly from enhanced interconnection. Therefore, long-term support for grid deployment requires a coherent legal framework and the fair distribution of costs and benefits.

The Presidency’s softening of the single competent authority model for cross-border projects is a pragmatic compromise, though it comes at a cost to developer certainty. Under the Commission’s original TEN-E proposal (2025c), a jointly designated unique point of contact would issue a single comprehensive decision for projects spanning two or more MS – a genuine consolidation of cross-border permitting. The Presidency (2026a) retains the joint contact point but makes the comprehensive decision explicitly non-binding, reframing it as a reference document that identifies and refers to the binding decisions of each MS’s national authority. This preserves MS sovereignty and is likely the only politically viable model given the constitutional constraints in several MS. However, developers of cross-border projects still face multiple binding national decisions with potentially divergent timelines, conditions and appeal procedures – the core coordination problem that the single authority was intended to solve. While the non-binding comprehensive decision reduces the complexity of information access for developers, it does not resolve the underlying legal fragmentation. A stronger intermediate option would be to require MS to align timelines and procedural requirements for cross-border projects even if final decision-making authority remains national – delivering most of the coordination benefit without the sovereignty concerns.

5.5. Financing: Deploy funds more catalytically

On financing, MS are divided on three dimensions, as identified in the disagreement chapter: the scale of CEF-E funding, the eligibility of domestic grid reinforcements for CEF-E funding, and the broader financing mix. The Presidency TEN-E compromise does not introduce any substantive changes to the eligibility conditions or the domestic investment exclusion.

The CEF-E eligibility criteria should be extended to include domestic grid reinforcements that are a prerequisite for cross-border capacity, and the targeting criteria should be refined. Under the current framework, CEF-E grants require a prior CBCA decision under Article 17 for works, which excludes purely domestic investments. This is the core of France’s objection: transit-driven domestic reinforcements generate real costs but receive no EU support because they fall outside the CBCA scope. The solution is to make CEF-E funding available for domestic grid investments where a structured assessment – of the kind proposed in the cost-sharing section above – establishes a causal link to cross-border capacity.

Beyond expanding the eligibility perimeter, CEF-E funds should also be deployed more catalytically, e.g. by prioritising projects with asymmetric cost-benefit profiles where costs accrue primarily to one of the parties, projects with the highest positive spillovers beyond the hosting MS where benefits accrue significantly to third-party countries, and bundles of combined projects where joint assessment reveals European-level value that individual projects would not demonstrate alone. This would improve both the fairness and the efficiency of EU infrastructure financing.

On the broader financing mix, more needs to follow. Despite the fivefold expansion of CEF-E funding, an estimated EUR 30 billion gap remains for electricity interconnection alone (Geneletti & Cremona 2025), and MS remain divided on how to close it. Sweden’s preference for capital market mobilisation stands in direct tension with the signals from France (and to some extent Germany), where President Macron and Bundesbank President Nagel have publicly expressed openness to Eurobonds. This divide cannot be resolved within the EU Grids Package (or the MFF) alone – it is ultimately a question of macro-financial architecture. However, progress is possible without reopening that debate: near-term instruments that do not require common debt – EIB direct lending and equity financing, national development bank models, and CEF-E grants – should be pursued first, while the broader question of common EU borrowing is addressed in parallel through the MFF negotiations.

Against this background, the CEIS rightly identifies the need to mobilise private capital, but its proposed instruments – securitisation facilities, hybrid bonds, and more specifically a EUR 500 million Sustainable Infrastructure Fund – are insufficient in scale relative to the overall investment challenge. German distribution system operators alone are expected to require around EUR 68 billion by 2035 (Agora Energiewende et al. 2026). The Commission’s premise that the investment need “far exceeds public funding capacity” should not be accepted uncritically: it risks foreclosing cheaper public options in favour of more complex private arrangements that carry higher costs and execution risk.

We will further explore financing strategies in a separate paper to be published in the coming weeks.

Bibliography

- 50hertz, Amprion, TenneT and TransnetBW (2026): “Position on the European Grids Package”,

- ACER (2026): “Congestion Revenues”

- Agora Energiewende / Stiftung Klimaneutralität / Dezernat Zukunft (2026): “Investitionen in eine zukunftsfähige Daseinsvorsorge. Aufschlüsselung nach Bundesländern”, p. 95

- Blenkisop, P. / Martinez, M. (2025): “Germany, Netherlands, Sweden Oppose EU Common Borrowing”.

- Büscher, M. / Dimitrisina, R. (2025): “Nordic Energy policies Sweden’s Challenges to the European Electricity Grid”, FES Just Climate

- Caulcutt, C. / Leali, G. (2026): “Macron Calls for Eurobonds Ahead of Informal Summit”, Politico.

- Cypriot Presidency (2026a): “Presidency Compromise Text on Proposal for a Regulation of the European Parliament and of the Council on Guidelines for Trans-European Energy Infrastructure, amending Regulations (EU) 2019/942, (EU) 2019/943 and (EU) 2024/1789 and repealing Regulation (EU) 2022/869”, EU Council,

- Cypriot Presidency (2026b): “Presidency Compromise Text on Proposal for a Directive of the European Parliament and of the Council amending Directives (EU) 2018/2001, (EU) 2019/944, (EU) 2024/1788 as regards acceleration of permit-granting procedure”, EU Council

- Emelianova, P. / Hoffmann-Willers, P. / Ruhnau, O. (2025): “Redistribution through Cross-Border Electricity Trade: How to Achieve Pareto Improvement?”, EWI Working Paper, (24), p. 43.

- Eurelectric (2025): “Electricity Data”.

- European Commission (Ed.) (2025a): “The Future of European Competitiveness: Part A: A Competitiveness Strategy for Europe”, Publications Office,

- European Commission (2025b): “European Grids”,

- European Commission (2025c): Proposal for a Regulation of the European Parliament and of the Council on Guidelines for Trans-European Energy Infrastructure, amending Regulations (EU) 2019/942, (EU) 2019/943 and (EU) 2024/1789 and repealing Regulation (EU) 2022/869.

- European Commission (2025d): Proposal for a Directive of the European Parliament and of the Council amending Directives (EU) 2018/2001, (EU) 2019/944, (EU) 2024/1788 as regards acceleration of permit-granting procedure.

- European Commission (2025e): “Energy Highways”.

- European Commission (2025f): Commission Notice – Guidance on Efficient and Timely Grid Connections.

- European Commission (2025g): Commission Guidance on the Design of Two-Way Contracts For Difference.

- European Commission (2025h): The Union List of Projects of Common Interest and Projects of Mutual Interest (‘Union list’), referred to in Article 3(4).

- European Commission (2025i): Proposal for a Regulation of the European Parliament and of the Council establishing the Connecting Europe Facility for the period 2028–2034, amending Regulation (EU) 2024/1679 and repealing Regulation (EU) 2021/1153.

- European Commission (2026): Clean Energy Investment Strategy.

- Eurostat (2025): “Share of electricity from renewables falls in early 2025”.

- Eurostat (2026): “Electricity Price Statistics”.

- Finesso, A. / Kralli, A. / Bene, C. / Goodall, F. / Bolscher, H. / Laan, J. van der / Volkova, L. / Ansarin, M. / Delzen, T. van / Andrey, C. / Jerphanion, G. de / Nana, O. / Ullmann, A. / Pschorr, E. / et al. (Eds.) (2025): Investment Needs of European Energy Infrastructure to Enable a Decarbonised Economy: Final Report, Luxembourg, Publications Office.

- Fraunhofer IEG / Fraunhofer ISI / d-fine (2025): “Integrated Infrastructure Planning and 2050 Climate Neutrality: Deriving Future-Proof European Energy Infrastructures”.

- Fuglsang, N. (2026): “DRAFT REPORT on the proposal for a directive of the European Parliament and of the Council amending Directives (EU) 2018/2001, (EU) 2019/944, (EU) 2024/1788 as regards acceleration of permit-granting procedures (COM(2025)1007 – C10-0341/2025 – 2025/0400(COD))”, European Parliament, Draft Report.

- Geneletti, G. / Cremona, E. (2025): “Money on the Line: Scaling Electricity Interconnection for Europe’s Energy Future”, p. 16.

- Heussaff, C. / Zachmann, G. (2025): “Upgrading Europe’s Electricity Grid Is About More Than Just Money”, Bruegel.

- Munster, B. / Camut, N. (2026): “France and Sweden Push to Kill Mechanism to Pay for Massive EU Grid Upgrades”, Politico.

- Roth, A. / Tagliapietra, S. / Zachmann, G. (2026): “Better Coordination for a More Efficient European Energy System”, Bruegel.

- Sigmund, T. (2026): “Euro-Bonds – Ein Bundesbank-Präsident auf Abwegen”.

- Stiewe, C. / Xu, A. L. / Eicke, A. / Hirth, L. (2025): “Cross-Border Cannibalization: Spillover Effects of Wind and Solar Energy on Interconnected European Electricity Markets”.

- TenneT (2026): “TenneT’s Position on the European Grids Package”, TenneT.

- TTE Council (2026): Transport, Telecommunications and Energy Council.

- Weber, I. (2023): “When and How to Use Price Controls? Towards Economic Disaster Preparedness”.